Commercial Vehicle Insurance: The Hidden Rules Every Owner Should Know.

Many people assume that insuring a commercial vehicle is the same as insuring a personal car. However, commercial vehicle insurance works very differently and often involves additional rules, risks, and coverage requirements. This is why many first-time commercial vehicle owners are surprised when they face insurance issues during a claim. Let's understand the key differences in simple terms.

MOTOR INSURANCE

Robin

6/16/20262 min read

🧾 What Is Commercial Vehicle Insurance?

Commercial vehicle insurance provides protection for vehicles used for business purposes.

These vehicles may include:

Trucks

Goods carriers

Taxis and cabs

School buses

Auto-rickshaws

Delivery vans

Passenger transport vehicles

Since these vehicles are used to earn income, they face different risks compared to private cars.

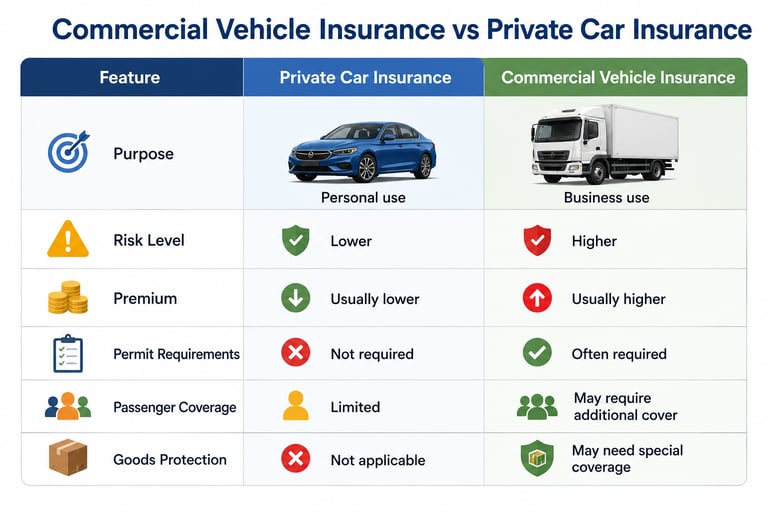

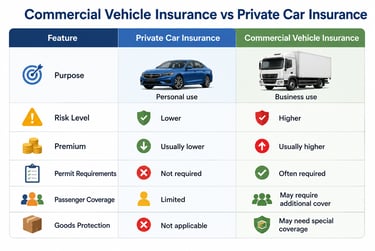

🚗 Commercial Vehicle vs. Private Car Insurance

⚠️ Why Commercial Vehicle Insurance Costs More

Commercial vehicles spend more time on the road and often travel longer distances.

This increases the chances of:

Accidents

Vehicle damage

Third-party claims

Theft

Passenger injuries

Cargo losses

Because the risk is higher, insurance premiums are usually higher than those for private vehicles.

Example

A family car may be driven a few hours each week.

A taxi or delivery vehicle may operate every day for several hours.

More usage means greater exposure to risk.

📜 Permit and Legal Requirements Matter

Many commercial vehicles require valid permits and licenses to operate legally.

Examples include:

Goods carriage permits

Passenger transport permits

Route permits

Driver commercial licenses

Why This Is Important

If a vehicle operates without the required permits or licenses, an insurance claim may face delays or even rejection.

Vehicle owners should always ensure that:

✅ Permits are valid

✅ Driver licenses are up to date

✅ Vehicle fitness certificates are maintained

🛡️ Third-Party Insurance Is Mandatory

Just like private vehicles, commercial vehicles must have third-party insurance.

This covers:

Injury to other people

Death of third parties

Damage to third-party property

However, third-party insurance does not cover damage to your own vehicle.

For broader protection, many owners choose comprehensive insurance.

🔧 Own Damage Cover Is Important

Own Damage (OD) coverage helps pay for repairs to your vehicle after:

Accidents

Natural disasters

Fire

Theft

Vandalism

Without OD coverage, the owner may have to pay repair costs from their own pocket.

Example

A truck worth ₹20 lakh is damaged in an accident.

Without Own Damage cover, the owner bears the repair expenses.

With proper insurance, eligible repair costs may be covered according to policy terms.

📦 Goods and Cargo May Need Separate Protection

A common misunderstanding is that vehicle insurance automatically covers the goods being transported.

In many cases, it does not.

Businesses may need additional cargo or goods-in-transit insurance to protect:

Inventory

Raw materials

Finished products

Valuable shipments

Example

A delivery truck carrying electronics meets with an accident.

The vehicle may be insured, but the damaged goods may require separate cargo insurance coverage.

👥 Passenger Coverage May Be Different

Commercial passenger vehicles such as taxis, buses, and school vehicles may require additional passenger liability coverage.

This helps provide protection if passengers are injured during an accident.

The coverage requirements depend on:

Vehicle type

Number of passengers

Regulatory requirements

❌ Why Claims Get Rejected

Many commercial vehicle claims are rejected due to avoidable mistakes.

Common reasons include:

Expired permits

Invalid driving licenses

Overloading

Unauthorized vehicle use

Incorrect information in the policy

Delay in claim reporting

Understanding policy conditions is extremely important.

💡 Tips for Commercial Vehicle Owners

To avoid problems during claims:

✅ Maintain valid permits and documents

✅ Ensure drivers have proper licenses

✅ Buy adequate insurance coverage

✅ Understand policy exclusions

✅ Report accidents immediately

✅ Review coverage regularly

🎯 Key Takeaways

Commercial vehicle insurance is different from private car insurance.

Premiums are higher because business vehicles face greater risks.

Valid permits and licenses are essential for claim eligibility.

Third-party insurance is mandatory but may not cover your own vehicle damage.

Goods being transported may need separate cargo insurance.

Understanding policy conditions can help prevent claim rejection.

Commercial vehicles are valuable business assets. The right insurance not only protects the vehicle but also helps keep your business running smoothly when unexpected events occur.