Factors Affecting Claim Ratio in General Insurance: A Simple Guide for Policyholders and Advisors.

Learn the key factors that influence claim ratios in general insurance, including accidents, natural disasters, inflation, underwriting, fraud, and claims management. Understand what claim ratios really mean for customers and advisors.

GENERALMOTOR INSURANCE

Robin

6/22/20262 min read

When customers buy insurance, one of the first questions they ask is:

"Will my claim be paid?"

This is where claim ratios become important.

A claim ratio provides insight into how an insurance company is handling claims and managing risks. However, many policyholders and even some advisors do not fully understand what influences these numbers.

Let's explore the key factors that affect claim ratios in general insurance.

🛡️ What is a Claim Ratio?

A claim ratio compares the amount paid by an insurer as claims against the premium collected during a specific period.

A high claim ratio may indicate that the insurer is paying a large portion of its premium income as claims.

A low claim ratio may suggest fewer claims or better risk management.

The claim ratio helps insurers evaluate profitability and sustainability.

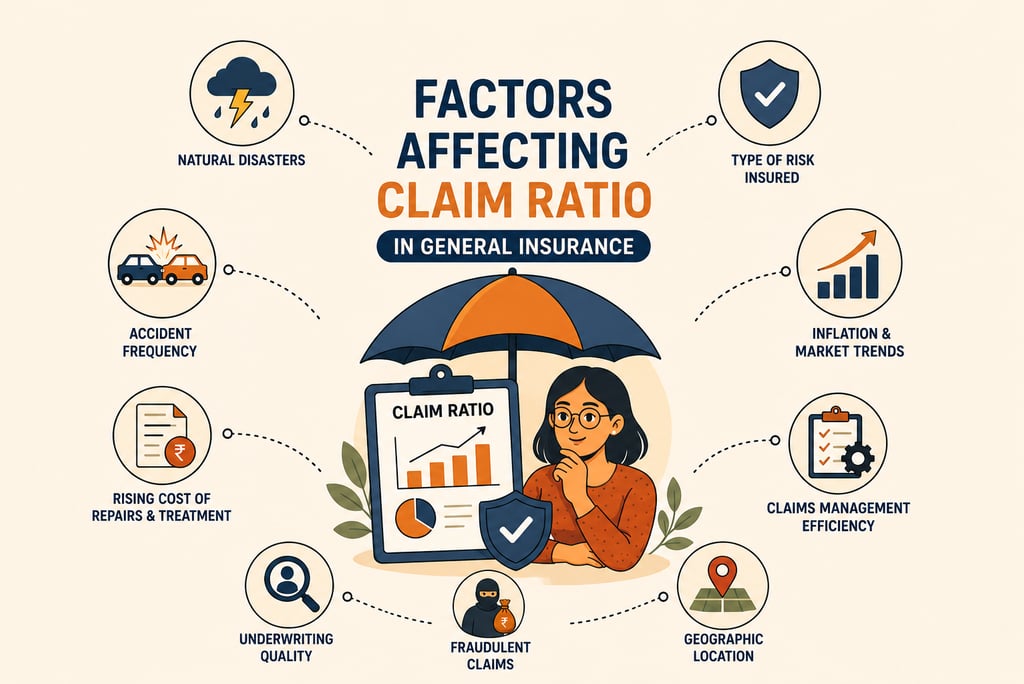

🚗 1. Type of Risk Insured

Different insurance products carry different levels of risk.

For example:

Health insurance generally experiences frequent claims.

Motor insurance sees regular accident-related claims.

Fire insurance may have fewer but larger claims.

Marine insurance depends on cargo and transit risks.

The nature of the risk directly affects claim frequency and claim amounts.

🌧️ 2. Natural Disasters and Catastrophic Events

Floods, cyclones, earthquakes, and other natural disasters can lead to a sudden increase in claims.

For example:

Heavy floods may damage thousands of vehicles.

Cyclones may affect homes, factories, and commercial properties.

During such events, claim ratios can rise significantly.

🚘 3. Increase in Accident Frequency

In motor insurance, claim ratios are influenced by:

Road conditions

Traffic density

Driver behavior

Vehicle usage

More accidents generally result in more claims and higher claim payouts.

🏥 4. Rising Cost of Repairs and Medical Treatment

Inflation affects insurance claims.

Examples include:

Higher vehicle repair costs

Expensive spare parts

Increased hospitalization expenses

Rising labour charges

Even if claim numbers remain the same, claim amounts may increase significantly.

📝 5. Underwriting Quality

Good underwriting helps insurers accept risks that fit their risk appetite.

Poor underwriting may lead to:

Higher claim frequency

Adverse selection

Increased losses

Insurers with strong underwriting practices often maintain healthier claim ratios.

⚠️ 6. Fraudulent Claims

Insurance fraud remains a major challenge.

Examples include:

Fake accidents

Inflated repair bills

Fabricated medical expenses

False property damage claims

Fraud increases claim costs and impacts overall claim ratios.

📍 7. Geographic Location

The location of the insured property or vehicle can affect claim experience.

Examples:

Flood-prone areas

Accident-prone roads

High-crime locations

Industrial zones with fire exposure

Higher risk locations often experience higher claim ratios.

🔄 8. Claims Management Efficiency

The speed and accuracy of claim handling also influence claim performance.

Efficient claims management can:

Detect fraud early

Reduce leakage

Improve customer satisfaction

Control claim costs

Modern insurers increasingly use technology and data analytics to improve claim handling.

🤝 Why This Matters for Insurance Advisors

Understanding claim ratios helps advisors:

✅ Recommend suitable insurers

✅ Explain premium differences

✅ Educate customers about risk factors

✅ Build credibility and trust

✅ Set realistic expectations regarding claims

Advisors should remember that a claim ratio alone does not determine whether an insurer is good or bad.

The context behind the numbers is equally important.

📈 What Customers Should Understand

A higher claim ratio is not always positive.

A lower claim ratio is not always negative.

Customers should also consider:

Claim settlement performance

Coverage offered

Customer service quality

Network garages or hospitals

Financial strength of the insurer

Insurance decisions should be based on a complete picture rather than a single statistic.

🎯 Key Takeaways

Claim ratio measures claims paid against premium earned.

Natural disasters, accidents, inflation, and fraud significantly impact claim ratios.

Good underwriting and efficient claims management help control losses.

Claim ratio is an important indicator but should not be viewed in isolation.

Advisors should help customers understand the story behind the numbers.

Final Thought

Claim ratios are like a health report for an insurance company. They provide useful insights, but they do not tell the entire story. A knowledgeable advisor understands the factors behind the numbers and helps customers make informed insurance decisions.