How Electric Vehicles (EVs) Are Transforming Motor Insurance

Imagine this: Your customer walks in excited about their shiny new electric car or bike. They love the zero fuel cost, smooth drive, and “green” feeling. But here’s what they don’t know yet — and what you can help them understand.

MOTOR INSURANCE

Robin

6/27/20263 min read

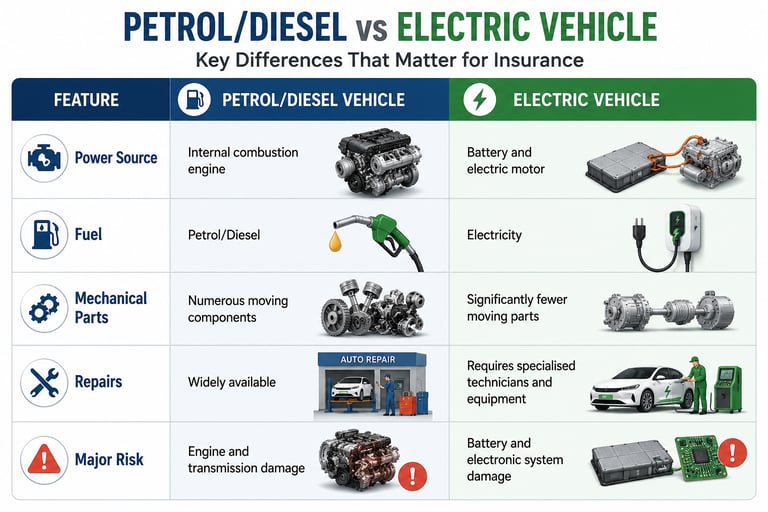

Although the basic principles of motor insurance remain the same, insuring an electric vehicle requires a different approach. The high-value battery, advanced electronics, charging infrastructure, and specialised repair processes have introduced entirely new risk considerations.

Why Electric Vehicles Are Different

Unlike conventional vehicles that rely on an internal combustion engine, EVs are powered by a rechargeable battery and an electric motor. This significantly changes the way insurers assess risks and calculate premiums.

These differences are gradually reshaping underwriting practices, claims management, and product design.

How EVs Are Transforming Motor Insurance

1. Battery Protection Has Become the Highest Priority

The battery is the single most expensive component of an electric vehicle, often accounting for 30% to 50% of its total value.

While a minor accident may cause limited external damage, it can affect the battery pack internally. Water ingress, impact damage, or thermal incidents may require costly repairs or even complete battery replacement.

For this reason, insurers now place significant emphasis on battery-related risks and suitable insurance coverage.

2. Fewer Claims but Higher Repair Costs

Electric vehicles generally have fewer moving parts than conventional vehicles, resulting in lower mechanical wear and reduced maintenance.

However, when repairs are required, they often involve specialised diagnostic equipment, trained technicians, and expensive replacement components.

As a result, insurers are experiencing:

Lower claim frequency

Higher average claim cost

This trend is changing the way premiums and risk models are designed.

3. Technology Risks Are Increasing

Modern EVs are equipped with sophisticated technology, including:

Advanced Driver Assistance Systems (ADAS)

Cameras and sensors

Connected vehicle software

Over-the-air software updates

While these technologies improve safety and convenience, they also introduce new risks such as software failures, sensor damage, and cybersecurity concerns that traditional motor insurance policies may not have been designed to address.

4. Quiet Operation Creates New Road Safety Challenges

Electric vehicles operate almost silently, particularly at low speeds.

Although this reduces noise pollution, pedestrians, cyclists, senior citizens, and children may not always hear an approaching EV, increasing the likelihood of low-speed collisions in residential areas and parking spaces.

This emerging risk is receiving greater attention from insurers and vehicle manufacturers.

5. Charging Infrastructure Introduces Additional Risks

Unlike conventional vehicles, EVs depend on charging equipment for daily operation.

Potential risks include:

Damage during charging

Faulty charging cables

Electrical faults

Home charging station incidents

Battery overheating

Fire-related losses

As EV adoption grows, insurers are expanding coverage options to address these evolving exposures.

6. Different Driving Patterns Influence Insurance Risk

Many EV owners primarily use their vehicles for urban commuting and shorter daily trips.

This results in:

More city driving

Increased stop-and-go traffic

Greater exposure to minor collisions

Reduced long-distance highway travel

These changing driving behaviours are influencing claims patterns and pricing strategies.

How Insurers Are Adapting

Insurance companies are redesigning products specifically for electric vehicles by introducing:

Battery protection cover

EV-specific add-on covers

Charging equipment protection

Roadside assistance for charging-related issues

Partnerships with authorised EV repair centres

Improved underwriting based on battery technology and vehicle features

These innovations ensure that insurance products remain aligned with the evolving needs of EV owners.

Tips for EV Owners When Buying Motor Insurance

Before purchasing an insurance policy for your electric vehicle, consider the following:

Ensure adequate battery protection.

Check whether charging equipment is covered.

Understand the claim process for battery damage.

Choose insurers with authorised EV repair networks.

Compare available EV-specific add-on covers before making a decision.

Selecting the right policy can significantly reduce financial risk in the event of an accident or battery-related loss.

Key Takeaway

Electric vehicles are not simply petrol cars with a different fuel source—they represent an entirely new category of mobility with unique insurance requirements.

As EV adoption continues to grow in India, motor insurance will increasingly focus on:

High-value battery protection

Advanced vehicle technology

Specialised repair networks

Charging-related risks

Updated underwriting models

Understanding these changes enables vehicle owners to choose appropriate insurance protection while helping insurance professionals provide informed guidance to customers.

The future of motor insurance is closely linked to the future of electric mobility, making EV insurance one of the fastest-evolving areas of the general insurance industry.