🌪️ How Insurance Companies Handle Catastrophic Losses

Natural disasters and large-scale events can cause thousands of insurance claims at the same time. Floods, earthquakes, cyclones, wildfires, and major industrial accidents can result in losses worth hundreds or even thousands of crores.

Yet insurance companies continue to pay claims and support policyholders during these difficult times.

How do they manage such massive financial challenges?

The answer lies in three important strategies:

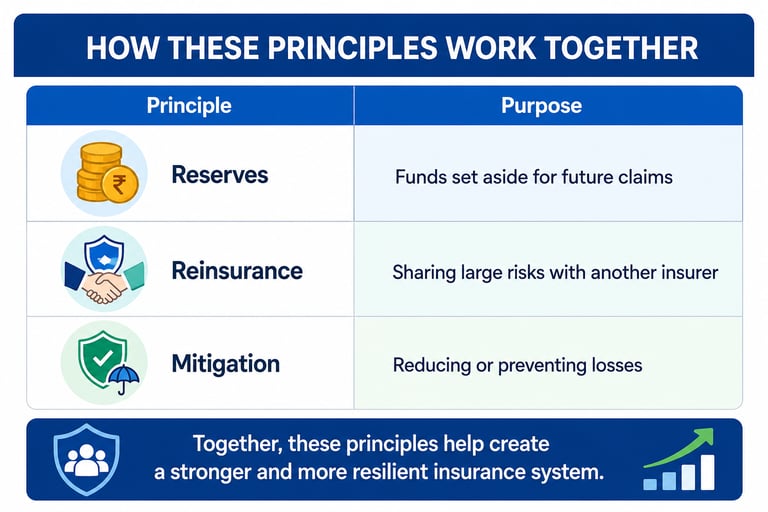

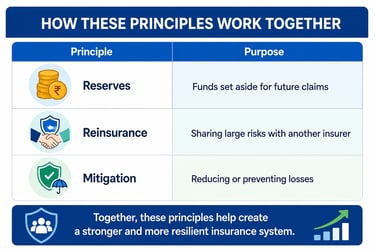

Reserves

Reinsurance

Mitigation

Together, these tools help insurers remain financially strong even during major disasters.

💰 Reserves – Funds Set Aside for Future Claims

Insurance companies do not spend all the premiums they collect.

A portion of the money is kept aside as reserves to meet future claim obligations.

These reserves act as a financial safety cushion.

Example

If a flood damages hundreds of homes in a city, insurers can use their reserves to start settling claims immediately.

Why It Matters

Reserves help insurers:

Pay claims quickly

Maintain financial stability

Meet regulatory requirements

Handle unexpected losses

Without adequate reserves, insurers would struggle during large claim events.

🛡️ Reinsurance – Sharing the Risk

Even large insurance companies cannot carry every risk alone.

To manage very large exposures, insurers purchase reinsurance.

Reinsurance is often called:

"Insurance for Insurance Companies."

Under this arrangement, part of the risk is transferred to another insurer called a reinsurer.

Example

A cyclone causes damage worth hundreds of crores.

Instead of bearing the entire loss alone, the insurer shares part of the claim burden with the reinsurer.

Why It Matters

Reinsurance helps insurers:

Handle very large claims

Protect financial strength

Continue serving customers

Increase their claim-paying capacity

🔥 Mitigation – Reducing Losses Before They Happen

Mitigation means taking steps to reduce the likelihood or severity of losses.

Insurance companies actively encourage risk prevention.

Examples

Fire safety inspections

Building safety standards

Flood protection measures

Driver safety programs

Workplace risk assessments

The goal is simple: Prevent losses whenever possible.

Why It Matters

Mitigation helps:

Reduce claim frequency

Lower claim severity

Improve public safety

Protect lives and property

The best claim is often the one that never occurs.

🌍 Real-World Example

Imagine a severe cyclone strikes a coastal region.

Thousands of homes, vehicles, and businesses suffer damage.

Reserves

Insurers use reserve funds to begin claim payments.

Reinsurance

Part of the financial burden is shared with reinsurers.

Mitigation

Buildings constructed using stronger safety standards may suffer less damage.

Together, these measures help insurers respond effectively while remaining financially stable.

🔗 How These Principles Work Together

Together, these principles help create a stronger and more resilient insurance system.

👨💼 Why Insurance Advisors Should Understand This

Understanding catastrophic loss management helps advisors:

✅ Explain insurer financial strength

✅ Build customer confidence

✅ Answer questions about claim-paying ability

✅ Improve insurance awareness

Customers often wonder how insurers can pay thousands of claims after a disaster. These three mechanisms provide the answer.

💬 Advisor Script Suggestion

"Insurance companies prepare for large disasters by maintaining reserves, sharing risks through reinsurance, and promoting loss prevention measures. These strategies help ensure claims can be paid even during major catastrophic events."

Simple and reassuring. ✅

🎯 Key Takeaways

Catastrophic losses can generate thousands of claims simultaneously.

Reserves provide immediate financial support for claim payments.

Reinsurance helps insurers share large risks.

Mitigation focuses on preventing or reducing losses.

Together, these strategies strengthen the insurance industry.

A financially strong insurance system benefits both insurers and policyholders.

While most policyholders never see these mechanisms in action, reserves, reinsurance, and mitigation work quietly behind the scenes to ensure insurance companies can continue protecting customers when disasters strike.