⚖️ Subrogation, Contribution, and Proximate Cause Explained

🌟 Introduction

In insurance, fairness is everything.

When a loss happens, the insurer compensates the insured — but only to the right extent, and from the right cause.

To make sure this fairness is maintained, insurance companies follow three key principles:

1️⃣ Subrogation

2️⃣ Contribution

3️⃣ Proximate Cause

Let’s understand each in plain, real-world language. 👇

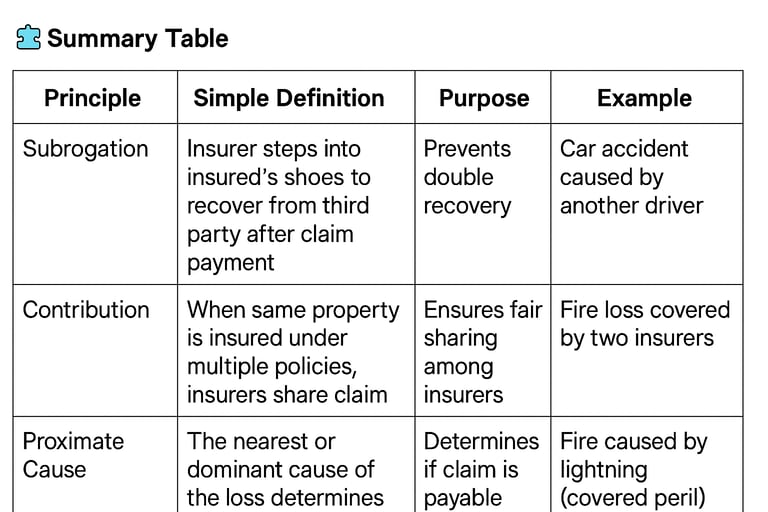

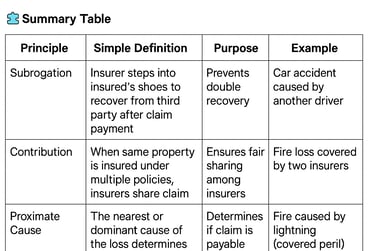

🔁 1. Subrogation – The Right to Recover

💬 Simple Meaning:

After paying a claim, the insurer steps into the shoes of the insured to recover money from the party who caused the loss.

It ensures the insured doesn’t get paid twice — once by the insurer and again from the guilty third party.

🏠 Example:

Ramesh’s car is hit by another vehicle.

His insurer pays ₹50,000 for the repairs.

Later, the insurer recovers that ₹50,000 from the person who caused the accident (the negligent driver).

That recovery right is Subrogation — the insurer’s right to act on behalf of the insured after claim payment.

⚖️ Why It’s Important:

✅ Prevents double recovery

✅ Holds the responsible party accountable

✅ Keeps insurance premiums fair

📘 Applies to:

All indemnity contracts (Fire, Marine, Motor), not to life or personal accident insurance.

🤝 2. Contribution – Sharing the Loss Fairly

💬 Simple Meaning:

If the same property is insured under multiple policies, all insurers share the claim proportionately.

It ensures no one insurer bears the full burden alone, and the insured doesn’t profit by claiming full compensation from more than one company.

🏠 Example:

A warehouse worth ₹10 lakh is insured with:

Insurer A for ₹6 lakh

Insurer B for ₹4 lakh

A fire causes ₹2 lakh loss.

👉 A will pay = (6/10) × 2,00,000 = ₹1,20,000

👉 B will pay = (4/10) × 2,00,000 = ₹80,000

Each insurer contributes in proportion to their coverage.

⚖️ Why It’s Important:

✅ Prevents unjust enrichment of the insured

✅ Distributes loss fairly among insurers

✅ Promotes balance and fairness in multi-policy situations

📘 Applies to:

All indemnity contracts — especially Fire and Marine Insurance.

🔍 3. Proximate Cause – Finding the Real Reason for the Loss

💬 Simple Meaning:

When several events happen together, the insurer looks for the dominant, effective, or nearest cause of the loss — that’s called the Proximate Cause.

If that cause is covered under the policy, the claim is payable.

If it’s excluded, the claim is not.

🏠 Example:

A house is damaged when:

Heavy rain causes flooding,

The flood leads to a short circuit,

The short circuit causes fire.

If the policy covers fire but excludes flood — the claim will still be paid, because fire (the proximate cause) was the direct cause of damage.

But if the property was damaged only by flood water, the claim would be rejected (flood = excluded peril).

⚖️ Why It’s Important:

✅ Helps determine whether a claim is payable or not

✅ Avoids confusion when multiple causes are involved

✅ Ensures insurers pay only for covered perils

📘 Applies to:

All types of insurance where loss has multiple contributing factors — fire, marine, motor, etc.

🧠 Quick Recap

Subrogation = Recovering from third party after payment

Contribution = Sharing loss among multiple insurers

Proximate Cause = Finding the main cause of loss

All three ensure the insurance system stays fair, balanced, and true to the principle of indemnity.

💡 Key Takeaways for Agents

✅ Always explain to clients that insurance pays for genuine losses only — no profit, no double claim.

✅ Understand the “cause and effect” — crucial for claim handling.

✅ Remember for exams:

“Subrogation, Contribution, and Proximate Cause uphold the fairness of indemnity insurance.”

✅ Use simple analogies — like car accidents, fire damage, or flood examples — to explain to clients.