🤝 Utmost Good Faith – Building Trust in Insurance Contracts

🌟 Introduction

Insurance isn’t built on bricks and mortar — it’s built on trust.

When you buy insurance, you’re asking a company to protect you from future losses you can’t even predict. The insurer, in turn, promises to pay when something goes wrong — based purely on the information you provide.

This mutual trust forms the foundation of the insurance relationship — and it’s called the Principle of Utmost Good Faith.

🔍 What is Utmost Good Faith?

The phrase “Utmost Good Faith” comes from the Latin term “uberrimae fidei.”

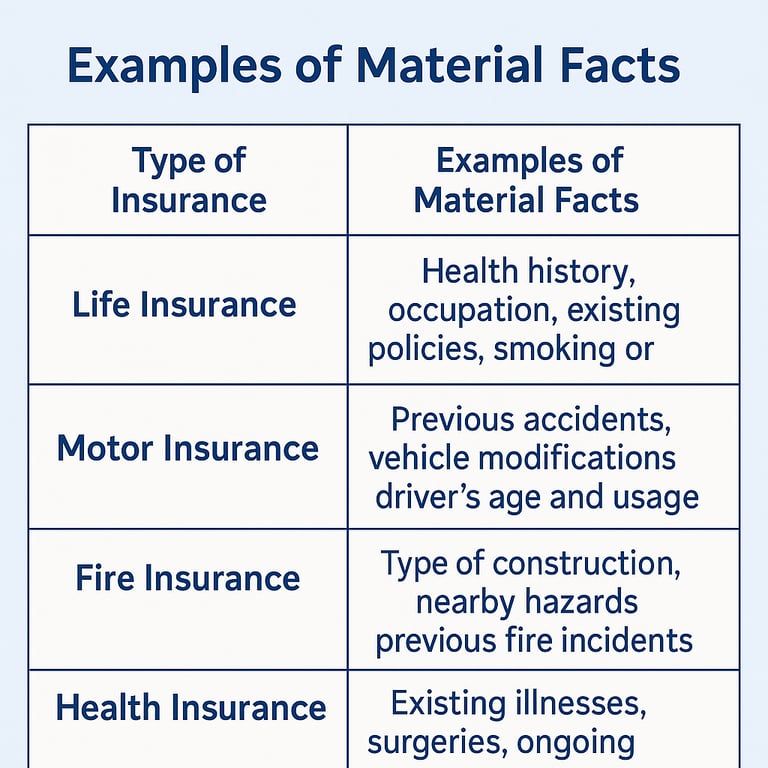

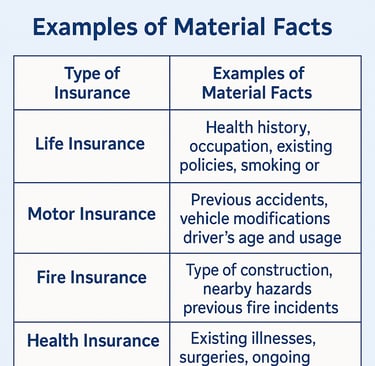

It means both the insurer and the insured must act with complete honesty and disclose all material facts that could affect the insurance contract.

In simple words:

“You must tell the truth — the whole truth — even if not asked directly.”

This principle applies to both parties:

The insured must disclose all facts that might affect the insurer’s decision to accept the risk.

The insurer must explain all policy terms, conditions, and exclusions clearly.

🏦 Why Is It So Important?

Unlike buying goods, where you can see what you’re getting, insurance is based on invisible promises.

The insurer depends completely on what the insured says about the risk.

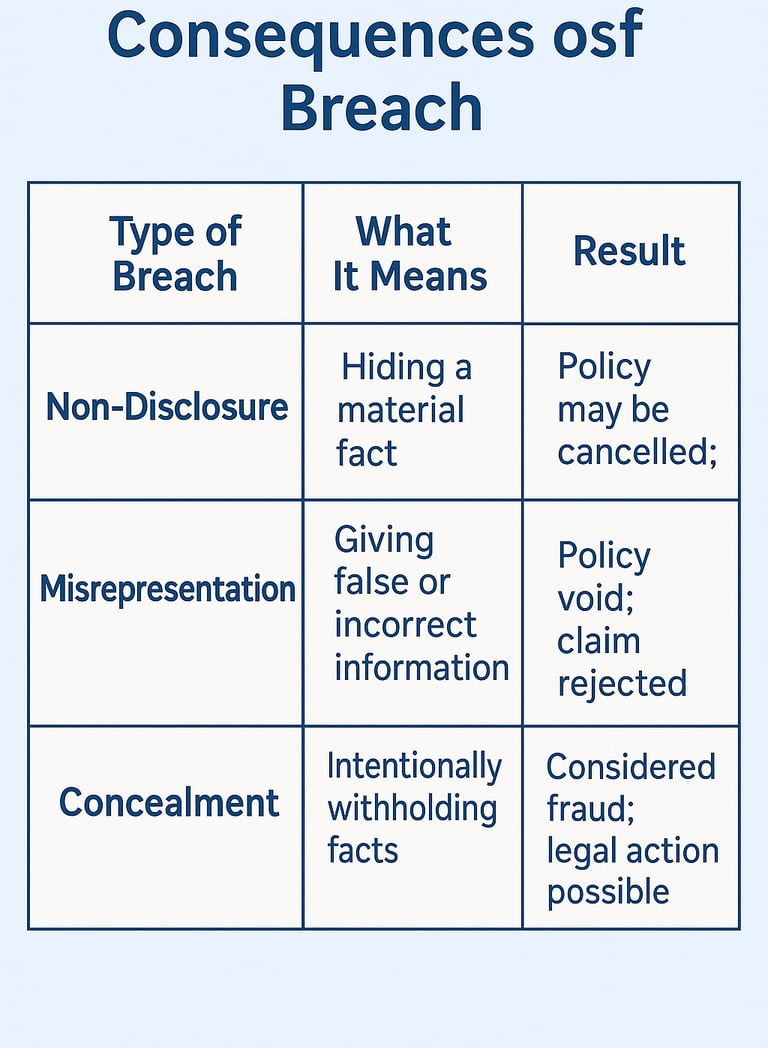

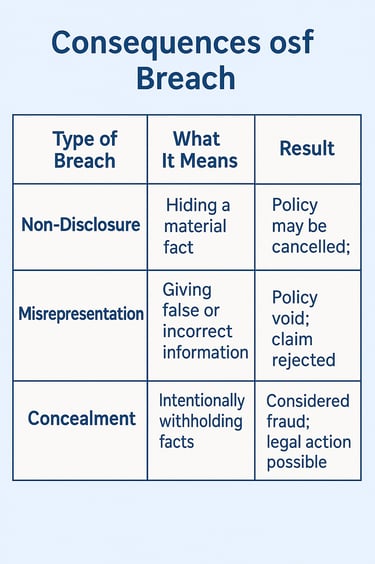

If any important detail is hidden or misrepresented, it can invalidate the entire contract.

The principle ensures:

✅ Transparency

✅ Fairness

✅ Proper risk assessment

✅ Avoidance of fraud and disputes

If such facts are hidden, it’s called non-disclosure or misrepresentation — and the insurer may reject claims or cancel the policy.

⚖️ How the Principle Works

Let’s see both sides 👇

🧍♂️ 1. The Insured’s Duty

The insured must:

Disclose all relevant facts honestly.

Avoid withholding any detail that affects the risk.

Answer all proposal form questions truthfully.

🏢 2. The Insurer’s Duty

The insurer must:

Clearly explain policy conditions, exclusions, and benefits.

Not hide any limitation or clause that affects claim payment.

Issue documents in plain, understandable language.

So, good faith goes both ways — it’s not just the customer’s responsibility!

Example:

If a person hides a serious heart condition while taking life insurance and later dies due to that illness — the insurer can legally reject the claim.

💬 Real-Life Example

Mrs. Anjali buys a health insurance policy but fails to mention she had undergone surgery a year ago.

After a few months, she files a claim related to the same condition.

When the insurer reviews her medical history, they find the non-disclosure — and reject the claim.

👉 If she had disclosed it honestly, the insurer might have accepted the proposal with a small extra premium or exclusion — and the contract would’ve remained valid.

🧠 Quick Recap

Utmost Good Faith = Complete honesty between insurer and insured.

Both sides must disclose all material facts truthfully.

The insurer’s trust in the customer’s disclosure allows accurate premium calculation.

Hiding facts = Breach of trust = Policy can be cancelled or claim denied.

The principle ensures transparency, fairness, and trust in insurance.

💡 Key Takeaways for Agents

✅ Always explain this principle to clients in simple words:

“Tell everything honestly — even if it seems small. It can save your claim later.”

✅ Encourage clients to read policy documents and ask questions before signing.

✅ Be transparent yourself — clearly mention exclusions, waiting periods, and limitations.

✅ Remember for exams:

“Insurance contracts are based on Uberrima Fidei — Utmost Good Faith.”